| Liabilities | Amount ( Rs.) | Assets | Amount ( Rs.) |

| Trade Creditors | 45,000 | Cash | 750 |

| Bills Payable | 12,000 | Bank | 12,000 |

| MR. Arvind’s Loan | 7,500 | Stock | 7,500 |

| MR. Balbir’s Loan | 15,000 | Investments | 15,000 |

| Reserve Fund | 15,000 | Book Debts 30,000 | |

| Investments Fluctuation Reserve | 1,500 | Less: Provision for Doubtful Debts (3,000) | 27,000 |

| Capital A/c : | Building | 22,500 | |

| Arvind 15,000 | Plant | 30,000 | |

| Balbir 15,000 | 30,000 | Goodwill | 6,000 |

| Profit and Loss A/c | 5,250 | ||

| 1,26,000 | 1,26,000 |

The firm was dissolved on the above date under the following arrangement:

(a) Arvind promised to pay off MR. Arvind’s Loan and took Stock at Rs. 6,000.

(b) Balbir took half the Investments @ 10% discount.

(c) Book Debts realised Rs. 28,500.

(d) Trade Creditors and Bills Payable were due on average basis of one month after 31st March, but were paid immediately on 31st March @ 2% discount per annum.

(e) Plant realised Rs. 37,500; Building Rs. 60,000; Goodwill Rs. 9,000 and remaining Investments Rs. 6,750.

(f) An old typewriter, written off completely from the firm’s books, now estimated to realise Rs. 450. It was taken by Balbir at this estimated price.

(g) Realisation expenses were Rs. 1,500.

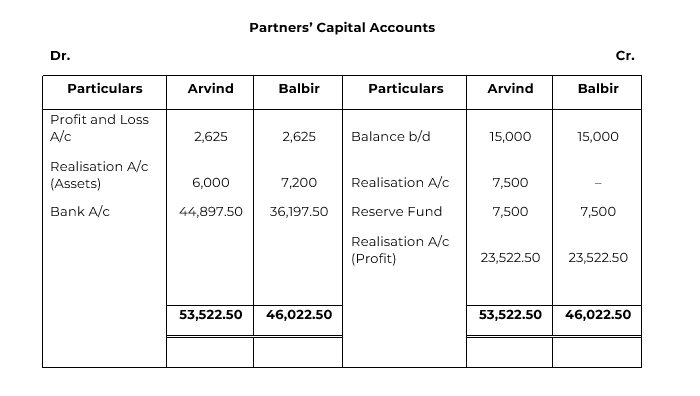

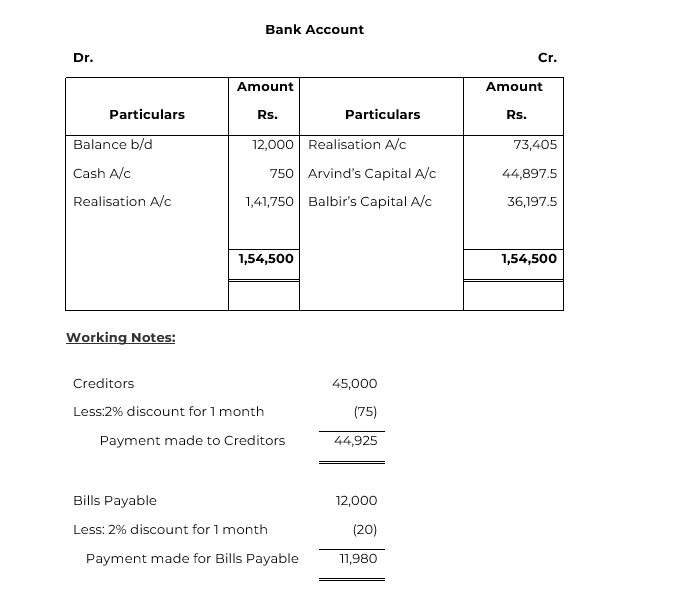

Show Realisation Account, Capital Accounts of Partners and Bank Account.

Solution