| Liabilities | Amount (Rs) | Assets | Amount (Rs) |

| Sundry Creditors | 40,000 | Goodwill | 25,000 |

| Bills Payable | 15,000 | Leasehold | 1,00,000 |

| Workmen Compensation Reserve | 30,000 | Patents | 30,000 |

| Capital A/c : | Machinery | 1,50,000 | |

| R –1,50,000 | Stock | 50,000 | |

| S – 1,25,000 | Debtors | 40,000 | |

| T – 75,000 | 3,50,000 | Cash at Bank | 40,000 |

| 4,35,000 | 4,35,000 |

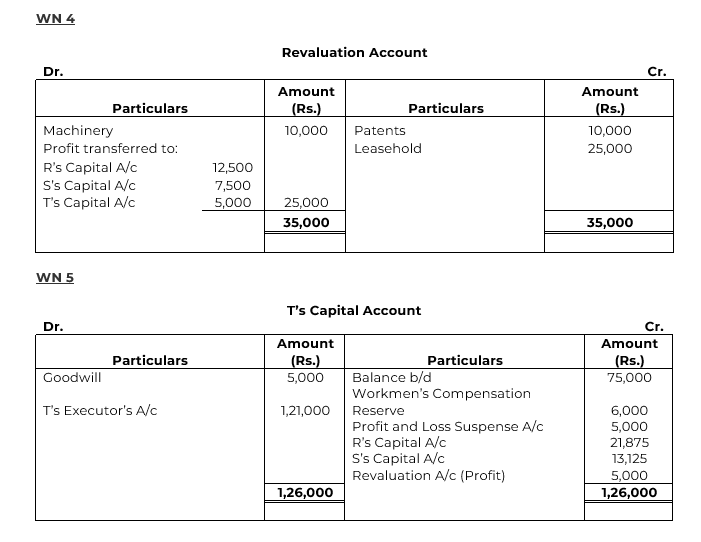

T died on 1st August, 2018. It was agreed that:

(a) Goodwill be valued at 212 years’ purchase of average of last 4 years’ profits which were: 2014-15: Rs. 65,000; 2015-16: Rs. 60,000; 2016-17: Rs. 80,000 and 2017-18: Rs. 75,000.

(b) Machinery be valued at Rs. 1,40,000; Patents be valued at Rs. 40,000; Leasehold be valued at Rs. 1,25,000 on 1st August, 2018.

(c) For the purpose of calculating T’s share in the profits of 2018-19, the profits in 2018-19 should be taken to have accrued on the same scale as in 2017-18.

(d) A sum of Rs. 21,000 to be paid immediately to the Executors of T and the balance to be paid in four equal half-yearly instalments together with interest @ 10% p.a.

Pass necessary Journal entries to record the above transactions and T’s Executors’ Account.

SOLUTION