| Liabilities | Amount ( Rs.) | Assets | Amount ( Rs.) |

| Creditors | 21,000 | Cash at Bank | 5,750 |

| Workmen Compensation Reserve | 12,000 | Debtors – 40,000 | |

| Investments Fluctuation Reserve | 6,000 | Less: Provision for Doubtful Debts – (2,000) | 38,000 |

| Capital A/c : | Stock | 30,000 | |

| X – 68,000 | Investment (Market Value Rs. 17,600) | 15,000 | |

| Y – 32,000 | Patents | 10,000 | |

| Z – 21,000 | 1,21,000 | Machinery | 50,000 |

| Goodwill | 6,000 | ||

| Advertisement Expenditure | 5,250 | ||

| 1,60,000 | 1,60,000 |

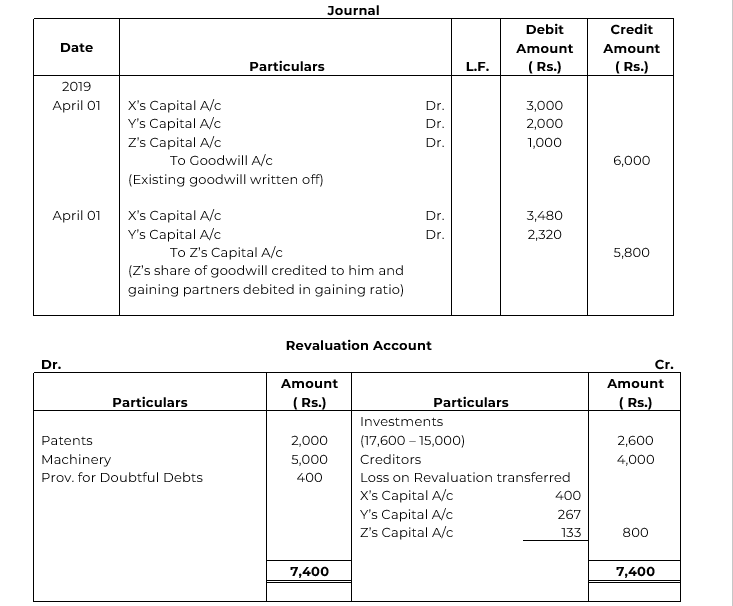

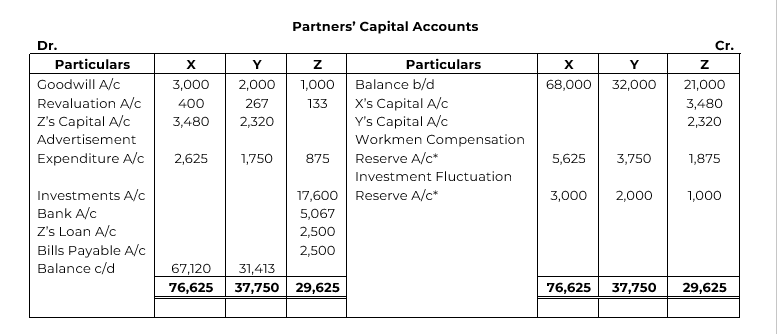

Z retired on 1st April, 2019 on the following terms:

(a) Goodwill of the firm is to be valued at Rs. 34,800.

(b) Value of Patents is to be reduced by 20% and that of machinery to 90%.

(c) Provision for doubtful debts is to be created @ 6% on debtors.

(d) Z took over the investment at market value.

(e) Liability for Workmen Compensation to the extent of Rs. 750 is to be created.

(f) A liability of Rs. 4,000 included in creditors is not to be paid.

(g) Amount due to Z to be paid as follows: Rs. 5,067 immediately, 50% of the balance within one year and the balance by a draft for 3 Months.

Give necessary Journal entries for the treatment of goodwill, prepare Revaluation Account, Capital Accounts and the Balance Sheet of the new firm.

SOLUTION