| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Sundry Creditors | 16,000 | Cash in Hand | 1,200 |

| Public Deposits | 61,000 | Cash at Bank | 2,800 |

| Bank Overdraft | 6,000 | Stock | 32,000 |

| Outstanding Liabilities | 2,000 | Prepaid Insurance | 1,000 |

| Capital A/c : | Sundry Debtors | 28,000 | |

| Deepika – 48,000 | Less: Provision for Doubtful Debts | 800 | |

| Rajshree – 40,000 | 88,000 | Plant and Machinery | 48,000 |

| Land and Building | 50,000 | ||

| Furniture | 10,000 | ||

| 1,73,000 | 1,73,000 |

On 1st April, 2019 the partners admit Anshu as a partner on the following terms:

(a) The new profit-sharing ratio of Deepika, Rajshree and Anshu will be 5 : 3 : 2 respectively.

(b) Anshu shall bring in Rs. 32,000 as his capital.

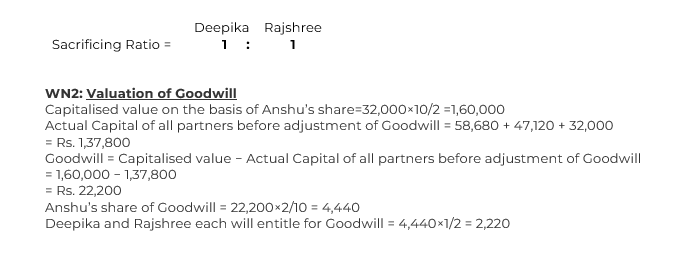

(c) Anshu is unable to bring in any cash for his share of goodwill. Partners, therefore, decide to calculate the goodwill on the basis of Anshu’s share in the profits and the capital contribution made by her to the firm.

(d) Plant and Machinery is to be valued at Rs. 60,000, Stock at Rs. 40,000 and the Provision for Doubtful Debts is to be maintained at Rs. 4,000. Value of Land and Building has appreciated by 20%. Furniture has been depreciated by 10%.

(e) There is an additional liability of Rs. 8,000 being outstanding salary payable to employees of the firm. This liability is not included in the outstanding liabilities, stated in the above Balance Sheet. Partners decide to show this liability in the books of account of the reconstituted firm.

Prepare Revaluation Account, Partners’ Capital Accounts and Balance Sheet of Deepika, Rajshree and Anshu.

SOLUTION