| Liabilities | Amount ( Rs.) | Assets | Amount ( Rs.) |

| Creditors | 1,65,000 | Cash | 1,20,000 |

| General Reserve | 90,000 | Debtors – 1,35,000 | |

| Capital A/c : | Less: Provision – (15,000) | 1,20,000 | |

| N – 2,25,000 | Stock | 1,50,000 | |

| S – 3,75,000 | Machinery | 4,50,000 | |

| G – 4,50,000 | 10,50,000 | Patents | 90,000 |

| Building | 3,00,000 | ||

| Profit and Loss Account | 75,000 | ||

| 13,05,000 | 13,05,000 |

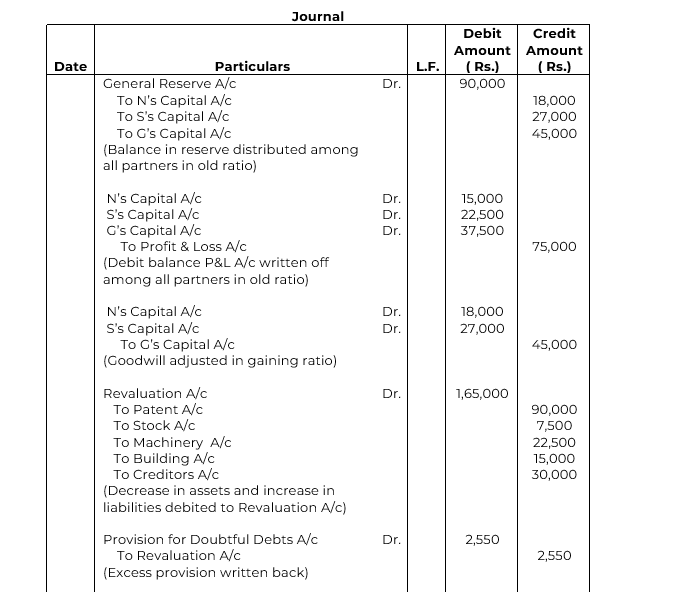

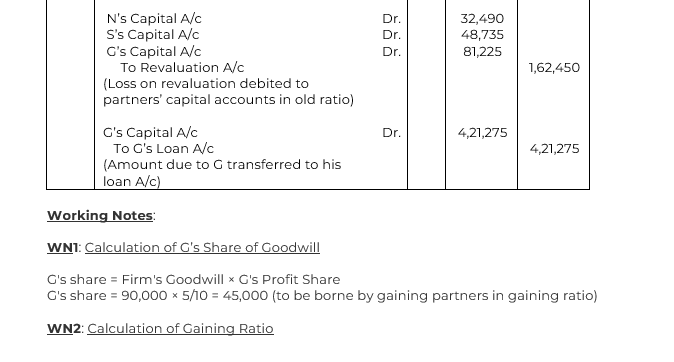

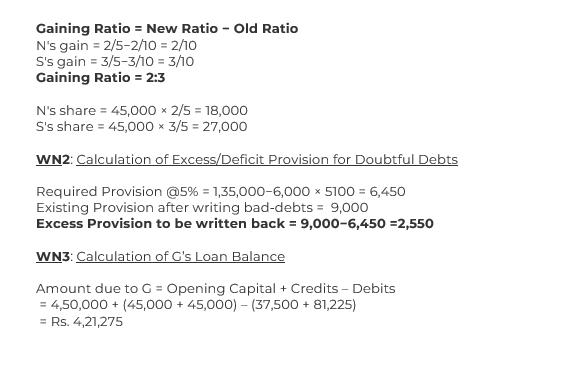

G retired on the above date and it was agreed that:

(a) Debtors of Rs. 6,000 will be written off as bad debts and a provision of 5% on debtors for bad and doubtful debts will be maintained.

(b) Patents will be completely written off and stock, machinery and building will be depreciated by 5%.

(c) An unrecorded creditor of Rs. 30,000 will be taken into account.

(d) N and S will share the future profits in 2 : 3 ratio.

(e) Goodwill of the firm on G’s retirement was valued at Rs. 90,000.

Pass necessary Journal entries for the above transactions in the books of the firm on G’s retirement.

SOLUTION