| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Capital A/c : | Land | 4,00,000 | |

| Yogesh – 5,00,000 | Building | 4,00,000 | |

| Naresh – 5,00,000 | 10,00,000 | Furniture | 50,000 |

| Current A/c : | Computers | 1,00,000 | |

| Yogesh – 1,10,000 | Stock | 1,50,000 | |

| Naresh – 90,000 | 2,00,000 | Sundry Debtors – 2,10,000 | |

| Employees’ Provident Fund | 25,000 | Less: Provision for Doubtful Debts – (10,000) | 2,00,000 |

| Workmen Compensation Reserve | 1,00,000 | Cash | |

| Sundry Creditors | 75,000 | Bank | 70,000 |

| Expenses Payable | 10,000 | Advertisement Suspense | 30,000 |

| 14,10,000 | 14,10,000 |

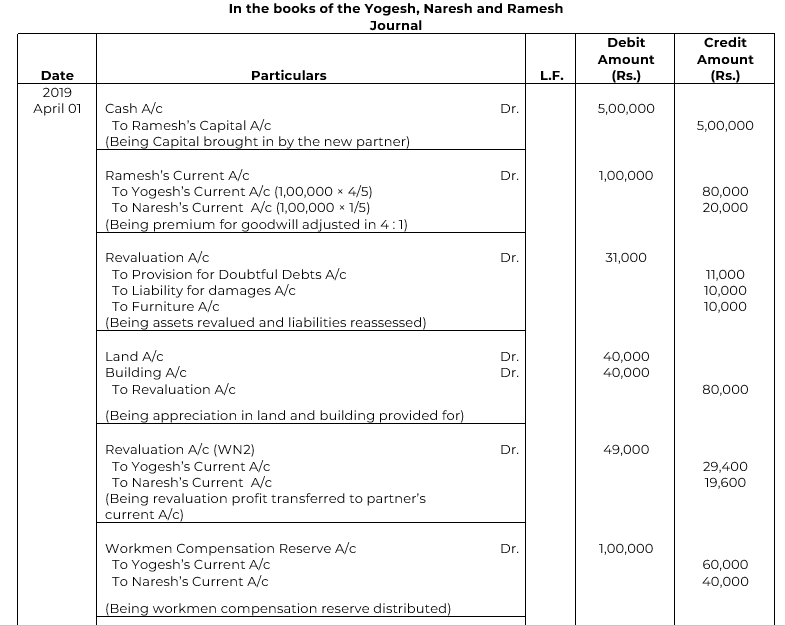

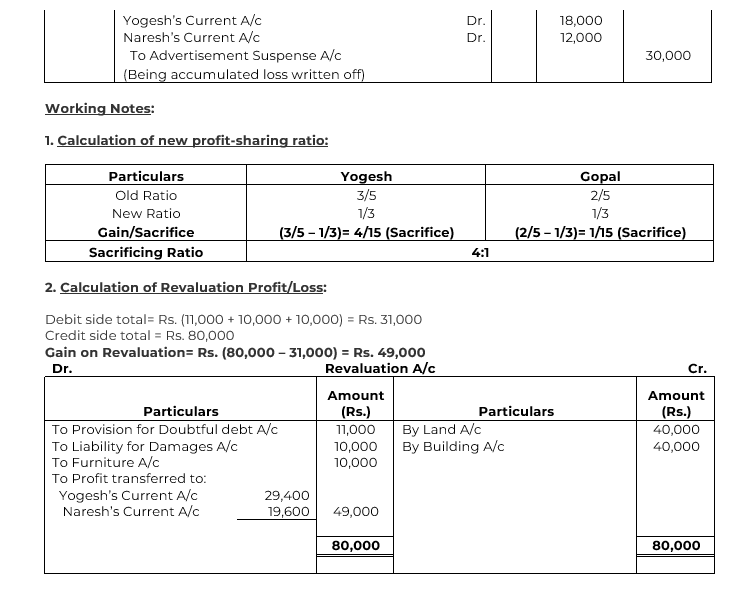

They admitted Ramesh on the following terms:

(a) He will bring Rs. 5,00,000 as his capital.

(b) His share of goodwill is valued at Rs. 1,00,000 but he is unable to bring cash for his share of goodwill. It is agreed to debit the amount to his Current Account.

(c) Value of Land and Building is to be appreciated by Rs. 40,000 each.

(d) Value of Furniture to be reduced to Rs. 40,000.

(e) Provision for Doubtful Debts to be increased to 10%.

(f) A liability for damages of Rs. 10,000 is to be created.

Pass the Journal entries on admission of Ramesh and prepare Revaluation Account.

SOLUTION