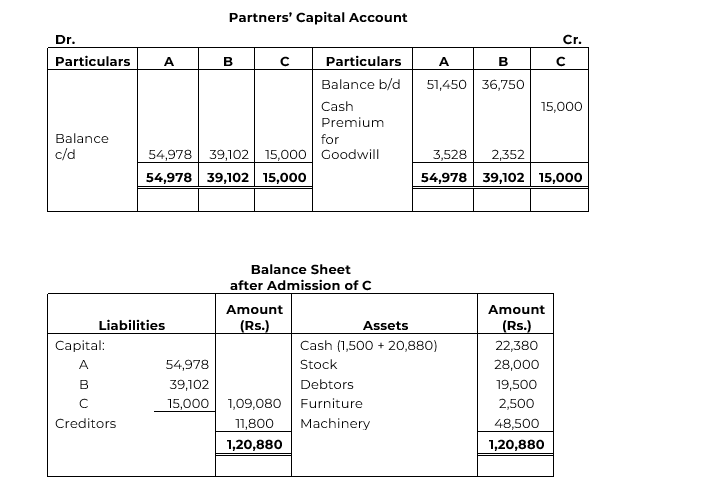

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Creditors | 11,800 | Cash | 1,500 |

| A’s Capital – 51,450 | Stock | 28,000 | |

| B’s Capital – 36,750 | 88,200 | Debtors | 19,500 |

| Furniture | 2,500 | ||

| Machinery | 48,500 | ||

| 1,00,000 | 1,00,000 |

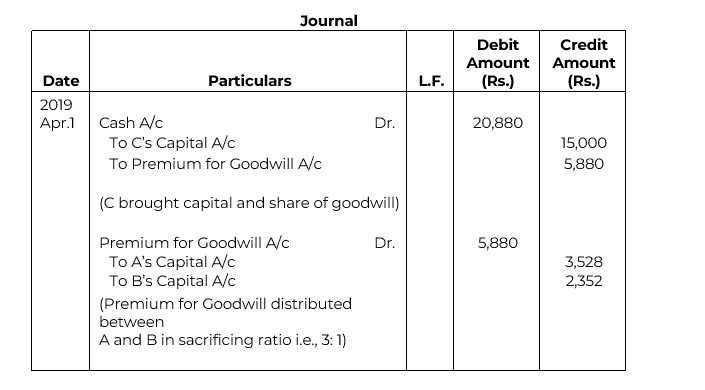

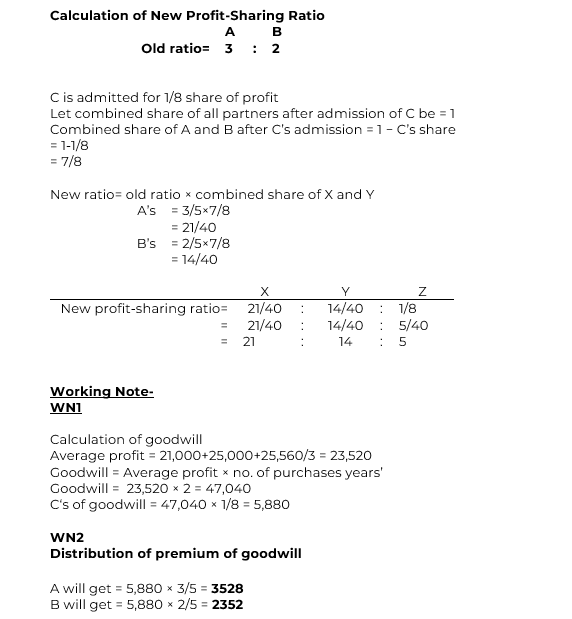

They admit C into partnership on 1st April, 2019 and give him 1/8th share in future profits on the following terms:

(a) Goodwill of the firm be valued at twice the average of the last three years’ profits which amounted to Rs. 21,000; Rs. 24,000 and Rs. 25,560.

(b) C is to bring cash for the amount of his share of goodwill.

(c) C is to bring cash Rs. 15,000 as his capital.

Pass Journal entries recording these transactions, draw out the Balance Sheet of the new firm and determine new profit-sharing ratio.

Solution