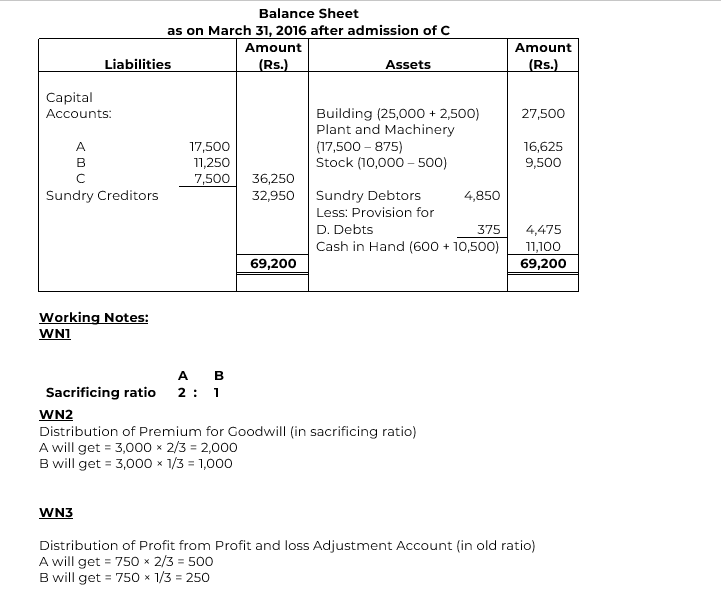

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Capital A/c : | Building | 25,000 | |

| A- 15,000 | Plant and Machinery | 17,500 | |

| B – 10,000 | 25,000 | Stock | 10,000 |

| Sundry Creditors | 32,950 | Sundry Debtors | 4,850 |

| Cash in Hand | 600 | ||

| 57,950 | 57,950 |

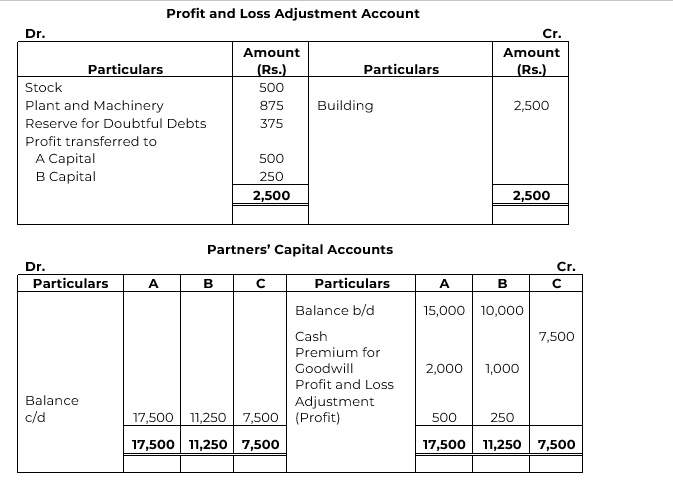

They admit C into partnership on the following terms:

(a) C was to bring Rs. 7,500 as his capital and Rs. 3,000 as goodwill for 1/4th share in the firm.

(b) Values of the Stock and Plant and Machinery were to be reduced by 5%.

(c) A Provision for Doubtful Debts was to be created in respect of Sundry Debtor Rs. 375.

(d) Building was to be appreciated by 10%.

Pass necessary Journal entries to give effect to the arrangements. Prepare Profit and Loss Adjustment Account (or Revaluation Account), Partners’ Capital Accounts and Balance Sheet of the new firm.

Solution