| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Creditors | 50,400 | Cash | 3,700 |

| Reserve | 12,000 | Stock | 20,100 |

| Capital A/cs: | Debtors | 62,600 | |

| A 40,000 | Loan to A | 10,000 | |

| B 25,000 | Investments | 16,000 | |

| C 15,000 | 80,000 | Furniture | 6,500 |

| Building | 23,500 | ||

| 1,42,400 | 1,42,400 |

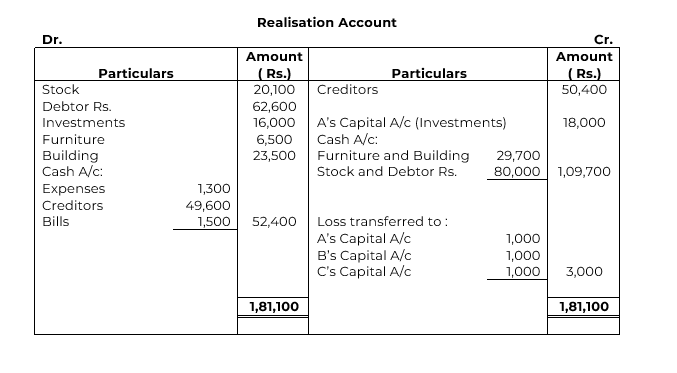

The firm was dissolved on the above date on the following terms:

(a) For the purpose of dissolution, Investments were valued at Rs. 18,000 and A took over the Investments at this value.

(b) Fixed Assets realised Rs. 29,700 whereas Stock and Debtors realised Rs. 80,000.

(c) Expenses of realisation amounted to Rs. 1,300.

(d) Creditors allowed a discount of Rs. 800.

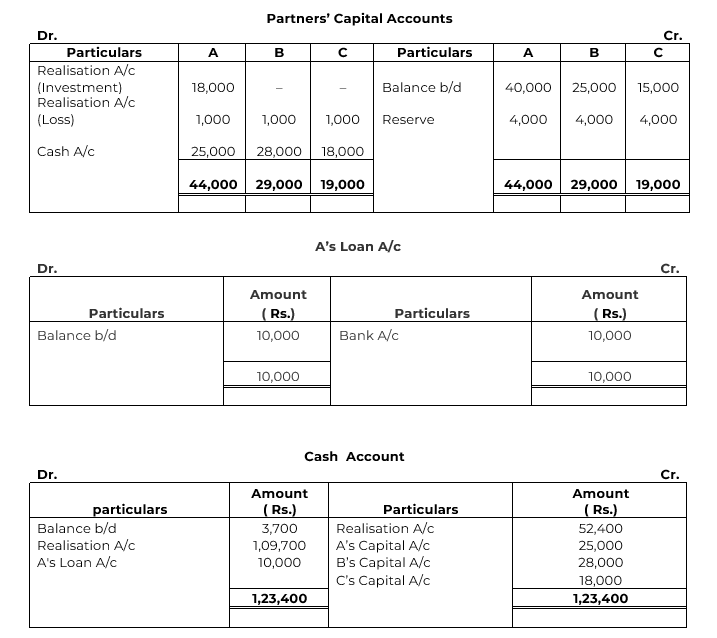

(e) One Bill receivable for Rs. 1,500 under discount was dishonoured as the acceptor had become insolvent and was unable to pay anything and hence the bill had to be met by the firm. Prepare Realisation Account, Partner’s Capital Accounts and Cash Account showing how the accounts would finally be settled among the partners.

Solution