| Liabilities | Amount ( Rs.) | Assets | Amount ( Rs.) |

| Creditors | 40,000 | Cash/Bank | 6,000 |

| Bills Payable | 40,000 | Investments | 30,000 |

| Naresh’s Loan | 44,000 | Debtors 40,000 | |

| Yogesh’s Loan | 42,000 | Less: Provision for Doubtful Debts (4,000) | 36,000 |

| Investment Fluctuation Reserve | 8,000 | Bills Receivable | 33,400 |

| Capital A/c : | Profit and Loss A/c | 1,10,600 | |

| Yogesh 21,000 | |||

| Naresh 21,000 | 42,000 | ||

| 2,16,000 | 2,16,000 |

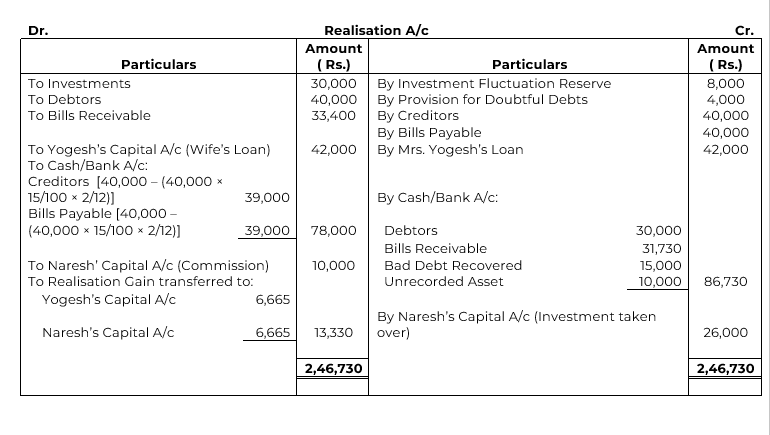

The firm was dissolved on following terms:

(a) Yogesh was to pay his wife’s loan.

(b) Debtors realised Rs. 30,000.

(c) Naresh was to take investments at an agreed value of Rs. 26,000.

(d) Creditors and Bills Payable were payable after two months but were paid immediately at a discount of 15% p.a.

(e) Bills Receivable were received allowing 5% rebate.

(f) A Debtor previously written off as Bad Debt paid Rs. 15,000.

(g) An unrecorded asset realised Rs. 10,000.

Prepare Realisation Account, Partners’ Capital Accounts, Partners’ Loan Account and Cash/Bank Account.

Solution